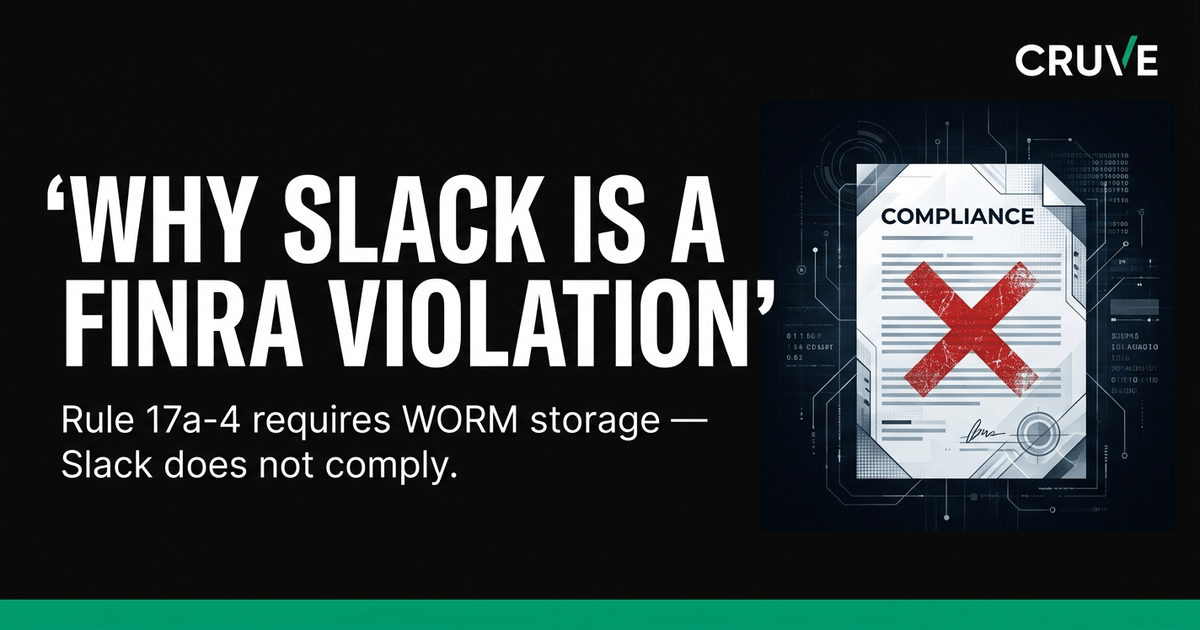

Why Slack Is a FINRA Violation Waiting to Happen

Slack is the communication platform of choice for thousands of financial firms. It's fast, flexible, and easy to deploy. It's also one of the most common sources of FINRA examination findings — and the gap between those two facts is exactly where compliance officers lose sleep.

The Problem Isn't Slack. It's What Slack Was Built For.

Slack was designed for technology companies and creative agencies. Its architecture, retention model, and data export capabilities reflect that origin. The platform stores messages in the cloud on Slack's infrastructure, provides limited and administratively cumbersome export tools, and offers retention controls that don't meet the specific requirements of FINRA Rule 17a-4.

That's not a criticism of Slack as a product. It's an engineering reality: Slack was built to make teams communicate faster, not to satisfy the record preservation requirements of the Securities Exchange Act of 1934.

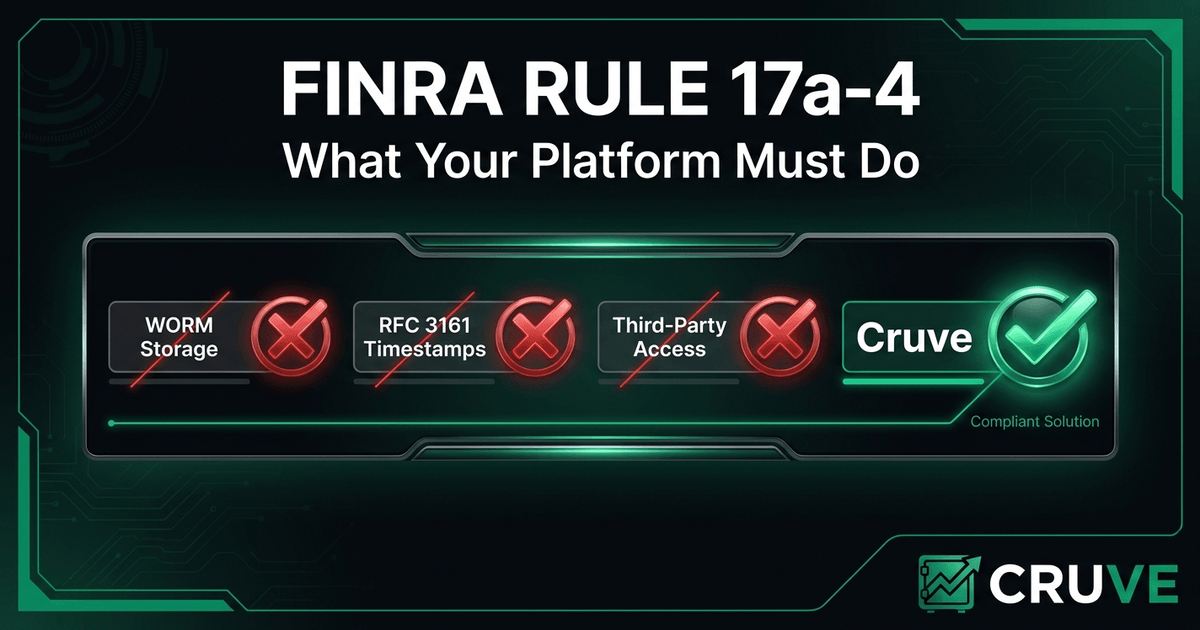

What FINRA Rule 17a-4 Actually Requires

Rule 17a-4 requires broker-dealers to preserve electronic communications in a non-rewriteable, non-erasable (WORM) format for a minimum of three years. The regulation specifies:

- Records must be stored in a format that cannot be altered or deleted during the retention period

- The firm must be able to produce records for regulatory examination within a reasonable time

- An independent third party must have access to the records — the "third-party download" requirement

- The storage system must include an index that can be searched and sorted

Slack's default configuration satisfies none of these requirements. Even with Slack's paid retention features enabled, you're relying on Slack's infrastructure — infrastructure you don't control, with retention policies that can be modified by administrators, and without the WORM compliance attestation that regulators require.

The Real Examination Risk

FINRA examiners have become increasingly sophisticated about messaging platforms. They know the difference between a firm that has a compliant archive and a firm that exports CSV files from Slack and calls it an archive. The examination questions have evolved accordingly.

During a routine communications review, examiners will typically ask: What electronic communications platforms are approved for business use? How are communications preserved in a WORM-compliant format? Who performs supervisory review of electronic communications? How does the firm detect use of unapproved platforms?

If your answer to the archiving question involves "we export from Slack periodically," you have a problem. Periodic exports create gaps. Exports are not WORM storage. And FINRA knows it.

The Third-Party Messaging Problem

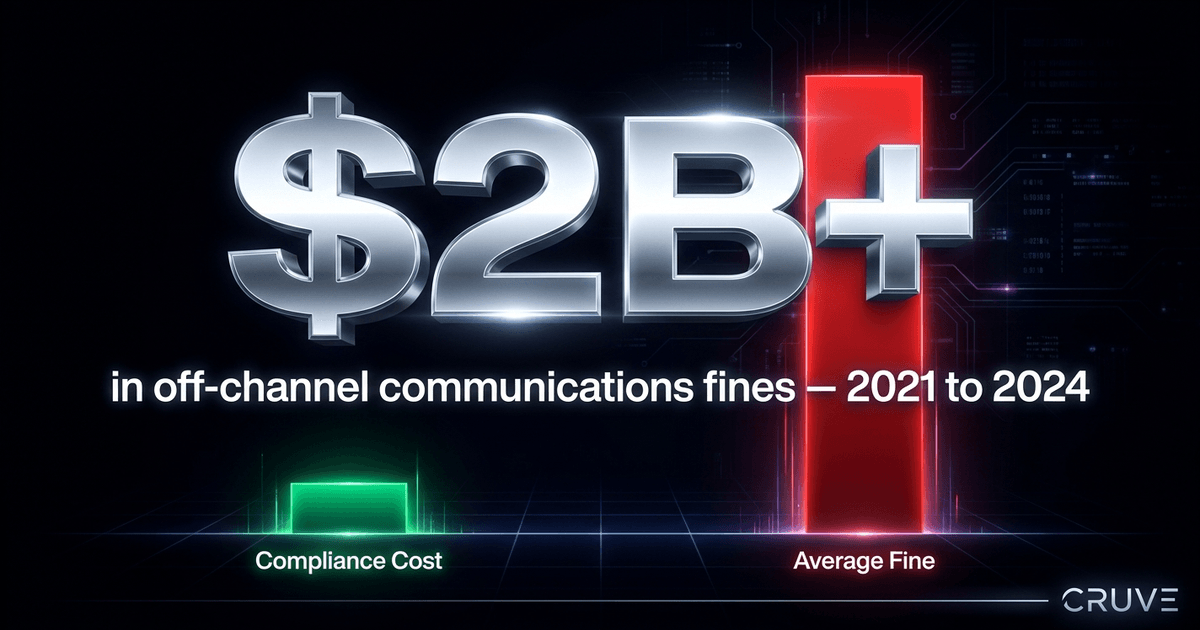

Slack's FINRA problem is compounded by what FINRA calls "off-channel" communications: business communications conducted on platforms that aren't approved or monitored by the firm. Text messages. WhatsApp. Signal. Personal email. The list is long and growing.

FINRA has made off-channel communications a top enforcement priority. Since 2021, major broker-dealers have paid collectively over $1.5 billion in fines — not for fraud, not for market manipulation, but for failing to preserve and supervise electronic communications conducted on platforms like WhatsApp and iMessage.

The firms fined weren't rogue operations. They were major institutions with sophisticated compliance programs. The problem wasn't bad intent — it was the practical reality that employees will use the fastest, most convenient communication tool available — and if that tool isn't compliant, the firm bears the regulatory cost.

What a Compliant Architecture Looks Like

A communications platform that genuinely satisfies FINRA Rule 17a-4 needs to do four things:

1. Capture every communication at the point of creation. Not through periodic export. Not through end-of-day batch processes. At the moment each message is sent, a cryptographically verifiable archive record is created.

2. Store records in genuine WORM format. WORM means write-once, read-many. The record cannot be modified or deleted before the retention period expires. AWS S3 Object Lock in COMPLIANCE mode is one implementation. What Slack calls "retention" is not.

3. Enable supervisory review. Rule 3110 requires principals to review communications. The archive must support efficient, structured review — not keyword search through exported CSV files.

4. Provide third-party access. Rule 17a-4 requires an independent third party to be able to access and download the records. This is a specific architectural requirement, not a general concept.

The Practical Question

The question for compliance officers isn't whether Slack violates FINRA rules — it does, in its default configuration, and arguably in its enhanced configuration as well. The question is what you do about it.

Overlay compliance solutions — products that sit on top of Slack and attempt to capture and archive communications — are one approach. They're better than nothing. But they introduce complexity, latency, and potential capture gaps, and they don't address the supervision workflow problem.

Purpose-built communications platforms — built from the ground up to satisfy 17a-4, 3110, and related requirements — are the other approach. More disruptive to deploy. But they solve the problem architecturally, not through patches.

The examiner who reviewed your Slack exports last cycle may not be the examiner who reviews them next time.

READY TO BUILD A COMPLIANT COMMUNICATIONS PROGRAM?

Cruve is purpose-built for FINRA and SEC-regulated firms — E2EE, WORM archiving, and supervisory review in one platform.

Request Early Access