FINRA Rule 17a-4: What Your Messaging Platform Must Do (And What It Probably Doesn't)

FINRA Rule 17a-4 is one of the most specific regulatory requirements in securities law. It doesn't just require that firms preserve records — it specifies the technical characteristics of the storage system. Most commercial messaging platforms, including platforms widely used by broker-dealers, don't satisfy those characteristics.

The Requirement in Precise Terms

Rule 17a-4(f) governs the electronic storage of records required under the Exchange Act. The core requirements:

- Records must be stored in a non-rewriteable, non-erasable format

- Records must be indexed and searchable

- Records must be accessible for examination within a reasonable time

- The system must include an audit trail recording when records were created, modified, and accessed

- An independent third party must have the ability to download a complete copy of all records on behalf of FINRA or the SEC

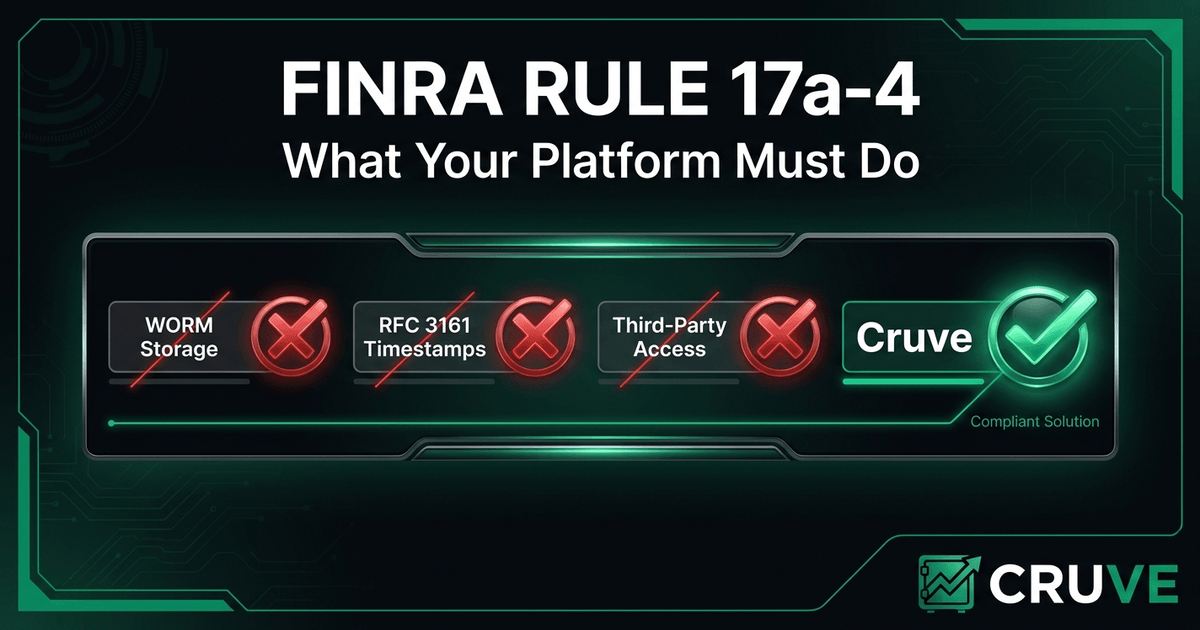

The "non-rewriteable, non-erasable" requirement is the technical heart of the rule. It means the storage system must be WORM-compliant: once a record is written, it cannot be modified or deleted until the retention period expires. This is not a policy requirement — it's an architectural requirement. The system must be technically incapable of modifying or deleting records during the retention period, not merely prohibited from doing so by policy.

What "Non-Rewriteable, Non-Erasable" Actually Means

WORM storage has a specific technical meaning that's often conflated with backup systems, retention policies, and archiving solutions that don't actually satisfy the standard.

True WORM storage means that the underlying storage medium or system prevents modification and deletion at the infrastructure level — not just at the application level. A database that has a "do not delete" flag on records is not WORM storage. An administrator with sufficient privileges can change that flag. AWS S3 Object Lock in COMPLIANCE mode is WORM storage; even AWS account administrators cannot delete or modify locked objects before the retention period expires.

This distinction matters because FINRA examiners have become sophisticated about the difference. A "compliance retention" feature that prevents normal users from deleting messages but allows administrators to modify retention settings is not WORM-compliant. FINRA has issued guidance on this point and examiners will probe it.

The Timestamp Requirement

Rule 17a-4 also requires that each archived record include a verifiable timestamp. This isn't just a date field that the application records — it's a cryptographically verifiable timestamp that proves when the record was created.

RFC 3161 timestamps — which involve a trusted timestamp authority signing a hash of the data with a timestamp — are the industry standard for satisfying this requirement. They provide non-repudiable proof that a record existed at a specific time, essential when records need to hold up under FINRA examination or legal discovery.

Most commercial messaging platforms don't use RFC 3161 timestamps. They record a server-side timestamp when the message is received, but that timestamp can be manipulated, is not cryptographically verifiable, and doesn't satisfy the evidentiary standard that regulators require.

The Third-Party Download Requirement

One of the most overlooked requirements of Rule 17a-4 is the third-party access requirement. The rule requires that the firm designate, in writing, an independent third party that has the technical ability to download a complete copy of all archived records on behalf of FINRA or the SEC.

This requirement exists to prevent situations where a firm's records are technically preserved but practically inaccessible to regulators because the firm controls the only means of access. The third-party designation creates an independent access path that regulators can use even if the firm is unable or unwilling to cooperate.

This is an architectural requirement, not just a contractual one. The third party must have actual technical access — not just a contractual right to request access. This means the storage system must be designed to support it.

The Supervision Corollary: Rule 3110

Rule 17a-4 covers preservation. Rule 3110 covers supervision. Together, they create the full compliance framework for electronic communications.

Rule 3110 requires each broker-dealer to establish and maintain a supervisory system that includes review of electronic communications by registered principal. The review must be reasonably designed to achieve compliance with applicable securities laws and regulations.

What does "reasonably designed" mean in practice? FINRA expects firms to demonstrate: who is responsible for reviewing which communications, how frequently reviews occur, what the firm does when non-compliant communications are identified, and how the firm detects communications on unapproved platforms.

This supervisory workflow requirement means that archiving alone isn't sufficient. The archive must support structured review — search by representative, by date range, by communication type, with the ability to flag, annotate, and escalate communications that require attention.

The Gap in Most Platforms

Most commercial messaging platforms, including those with "compliance" or "archiving" features, fall short of the full 17a-4 standard in at least one of three ways:

Storage architecture: Messages are stored in application databases that can be modified by administrators, or archived to standard cloud storage without WORM configuration.

Timestamp integrity: Timestamps are application-level records without cryptographic verification, making them potentially manipulable and insufficient as evidentiary records.

Access architecture: Third-party access is contractual, not technical — the vendor can grant access but hasn't built independent access paths into the storage architecture.

These aren't minor technical quibbles. They're the specific points that FINRA examiners focus on when reviewing a firm's compliance architecture. Firms that discover these gaps during an examination rather than before are in a significantly more difficult position.

Building a Compliant System

A communications platform that genuinely satisfies Rule 17a-4 needs to be designed around these requirements from the ground up. Retrofitting compliance onto a platform built for general-purpose communication consistently produces inadequate results.

The architectural requirements — WORM storage with true enforcement, RFC 3161 timestamps, independent third-party access, indexed and searchable records, supervisory review workflows — need to be core features of the platform, not afterthoughts bolted on through overlay products.

READY TO BUILD A COMPLIANT COMMUNICATIONS PROGRAM?

Cruve is purpose-built for FINRA and SEC-regulated firms — E2EE, WORM archiving, and supervisory review in one platform.

Request Early Access